Bankruptcy Lawyer

Imagine $220,000 of student debt disappearing at the sound of a gavel. In the Rosenberg bankruptcy case, a Navy vet with no disabilities and extenuating circumstances experienced just that. A New York bankruptcy judge ruled to discharge all $220,000 student debt because of her unprecedented interpretation of the phrase “undue burden”. With a student debt crisis looming over the horizon, many of us are wondering if this gavel smack was heard across the country.

New Precedent?

In order to know if this sets a new precedent, we need to visit the history of federal student loans. Remember the stories from your older relatives about the sweat and tears it took to work their way through college? Well, the money made at machine shops and dinners was enough to cover the average rate for college tuition.

The cost of college has surged at a much faster pace than overall inflation:

The first student loan programs were enacted during Lyndon Johnson’s “war on poverty.” They were created as a last resort for the neediest students. The programs increased demand for financial aid and compelled Congress to enact the Middle Income Student Assistance Act. MISAT made federal student loans available to students with less regard to need.

Keep in mind that these programs were created during a time when it was still possible to pay for tuition with some savings and part-time work.

The ubiquity of student loans compelled Congress to update the bankruptcy laws for student debt. In 1976, they passed the Education Amendments Act to prevent massive defaults in federal loans.

What happens when you broaden the access of credit to millions of people and make it almost impossible to not pay it back?

University spending and costs go up to stay competitive.

The EAA prohibited discharge of student loans in bankruptcy unless the debtor could establish undue hardship. Congress left the definition of undue hardship up to the courts.

Most courts use a student bankruptcy case from 1987 to set the guidelines for defining undue hardship:

Brunner v. NY HESC

(1) that the debtor cannot maintain, based on current income and expenses, a "minimal" standard of living for herself and her dependents if forced to repay the loans.

(2) that additional circumstances exist indicating that this state of affairs is likely to persist for a significant portion of the repayment period of the student loans.

(3) that the debtor has made good faith efforts to repay the loans.

Rosenberg v. NY SHES

In Rosenberg’s ruling, Judge Morris stated that she was applying the Brunner test as it was originally intended. She argued that the standard was misapplied for 32 years.

Courts have made a habit of focusing on the causes preventing the debtor from paying their loans. They require evidence that demonstrates that some extenuating circumstance is the primary cause of this inability.

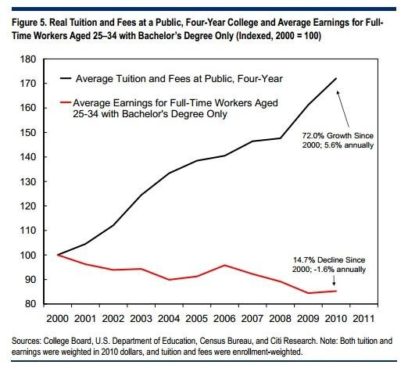

This standard was set with the assumption that, when applied responsibly, student loans would improve financial prospects. At the time of the Brunner case, this was a reasonable assumption. The average wage for college graduates was proportional to the cost of education. This chart from 2000-2010 demonstrates a clear divergence from that norm:

There is now serious reason to doubt the efficacy of higher education. The total student loan debt just passed 1.5 Trillion and many people are seriously doubting their choice to go to college.

The years Mr. Rosenberg spent struggling to pay back his loans is enough evidence to suggest that the system is broken. Judge Morris saw this as a straight forward case. Instead of focusing on justifying Rosenberg’s inability to use his degree to make enough money to pay off his debt, Morris focused on the evidence suggesting that Rosenberg could not maintain a minimal standard of living with the debt he incurred. Morris cited this approach as the correct reading of the Brunner case and then followed with a list of previous cases that failed to interpret this standard correctly.

The strongest piece of evidence for Mr. Rosenberg bankruptcy case was his negative income of about $1,500 each month. This was an undue burden because it demonstrated that Rosenberg could not maintain a minimal standard of living. It is safe to assume that Rosenberg is not alone. There are probably countless others not able to make the minimum loan payments with their current salary. Many are letting the interest balloon and double their debt because they assume that bankruptcy is not an option.

When you read the Brunner case through the lens of rising college debt and stagnating wages, assumptions about fault and blame change. The EAA is a large reason why tuition costs ballooned the way they did. On top of that, many students were promised that investing in a degree would yield the same results it did for the previous generation. You should no longer need to prove that extenuating circumstances prevented you from paying the debt, when that is obviously no longer the exception. There is something fundamentally wrong with higher education and it is time that courts start to recognize that. The Rosenberg case could be the ruling that sets a new precedent.

Bankruptcy Lawyer

Imagine $220,000 of student debt disappearing at the sound of a gavel. In the Rosenberg bankruptcy case, a Navy vet with no disabilities and extenuating circumstances experienced just that. A New York bankruptcy judge ruled to discharge all $220,000 student debt because of her unprecedented interpretation of the phrase “undue burden”. With a student debt crisis looming over the horizon, many of us are wondering if this gavel smack was heard across the country.

New Precedent?

In order to know if this sets a new precedent, we need to visit the history of federal student loans. Remember the stories from your older relatives about the sweat and tears it took to work their way through college? Well, the money made at machine shops and dinners was enough to cover the average rate for college tuition.

The cost of college has surged at a much faster pace than overall inflation:

The first student loan programs were enacted during Lyndon Johnson’s “war on poverty.” They were created as a last resort for the neediest students. The programs increased demand for financial aid and compelled Congress to enact the Middle Income Student Assistance Act. MISAT made federal student loans available to students with less regard to need.

Keep in mind that these programs were created during a time when it was still possible to pay for tuition with some savings and part-time work.

The ubiquity of student loans compelled Congress to update the bankruptcy laws for student debt. In 1976, they passed the Education Amendments Act to prevent massive defaults in federal loans.

What happens when you broaden the access of credit to millions of people and make it almost impossible to not pay it back?

University spending and costs go up to stay competitive.

The EAA prohibited discharge of student loans in bankruptcy unless the debtor could establish undue hardship. Congress left the definition of undue hardship up to the courts.

Most courts use a student bankruptcy case from 1987 to set the guidelines for defining undue hardship:

Brunner v. NY HESC

(1) that the debtor cannot maintain, based on current income and expenses, a “minimal” standard of living for herself and her dependents if forced to repay the loans.

(2) that additional circumstances exist indicating that this state of affairs is likely to persist for a significant portion of the repayment period of the student loans.

(3) that the debtor has made good faith efforts to repay the loans.

Rosenberg v. NY SHES

In Rosenberg’s ruling, Judge Morris stated that she was applying the Brunner test as it was originally intended. She argued that the standard was misapplied for 32 years.

Courts have made a habit of focusing on the causes preventing the debtor from paying their loans. They require evidence that demonstrates that some extenuating circumstance is the primary cause of this inability.

This standard was set with the assumption that, when applied responsibly, student loans would improve financial prospects. At the time of the Brunner case, this was a reasonable assumption. The average wage for college graduates was proportional to the cost of education. This chart from 2000-2010 demonstrates a clear divergence from that norm:

There is now serious reason to doubt the efficacy of higher education. The total student loan debt just passed 1.5 Trillion and many people are seriously doubting their choice to go to college.

The years Mr. Rosenberg spent struggling to pay back his loans is enough evidence to suggest that the system is broken. Judge Morris saw this as a straight forward case. Instead of focusing on justifying Rosenberg’s inability to use his degree to make enough money to pay off his debt, Morris focused on the evidence suggesting that Rosenberg could not maintain a minimal standard of living with the debt he incurred. Morris cited this approach as the correct reading of the Brunner case and then followed with a list of previous cases that failed to interpret this standard correctly.

The strongest piece of evidence for Mr. Rosenberg bankruptcy case was his negative income of about $1,500 each month. This was an undue burden because it demonstrated that Rosenberg could not maintain a minimal standard of living. It is safe to assume that Rosenberg is not alone. There are probably countless others not able to make the minimum loan payments with their current salary. Many are letting the interest balloon and double their debt because they assume that bankruptcy is not an option.

When you read the Brunner case through the lens of rising college debt and stagnating wages, assumptions about fault and blame change. The EAA is a large reason why tuition costs ballooned the way they did. On top of that, many students were promised that investing in a degree would yield the same results it did for the previous generation. You should no longer need to prove that extenuating circumstances prevented you from paying the debt, when that is obviously no longer the exception. There is something fundamentally wrong with higher education and it is time that courts start to recognize that. The Rosenberg case could be the ruling that sets a new precedent.